Contact: Brenon Daly

As we look back on 2017 and ahead to 2018, 451 Research has published its annual forecast for tech M&A, highlighting the trends that we expect to shape deal flow and the markets that we think will see much of the activity. The 2018 Tech M&A Outlook – Introduction serves as an overview of the broad M&A market, setting the stage for the upcoming publication of our comprehensive report that features analysis and predictions for eight specific IT markets on what deals are likely in 2018.

The full report, which we think of as an ‘M&A playbook’ for the enterprise IT market, has insightful forecasts for activity in application software, information security, mobility and other key sectors. The 80-plus-page 2018 Tech M&A Outlook report will be published at the end of January. It will be available at no additional cost for subscribers to 451 Research’s M&A KnowledgeBase Professional and Premium products, and will be available for purchase for 451 Research clients and others that don’t subscribe to our M&A KnowledgeBase products. (If you’re interested in purchasing the full 80-plus-page report, contact your account manager or click here.)

In the meantime, our introduction provides insights on some of the overall dealmaking trends that are also likely to shape activity and valuations in sector-specific transactions. Key highlights in our overview of the broader M&A market include:

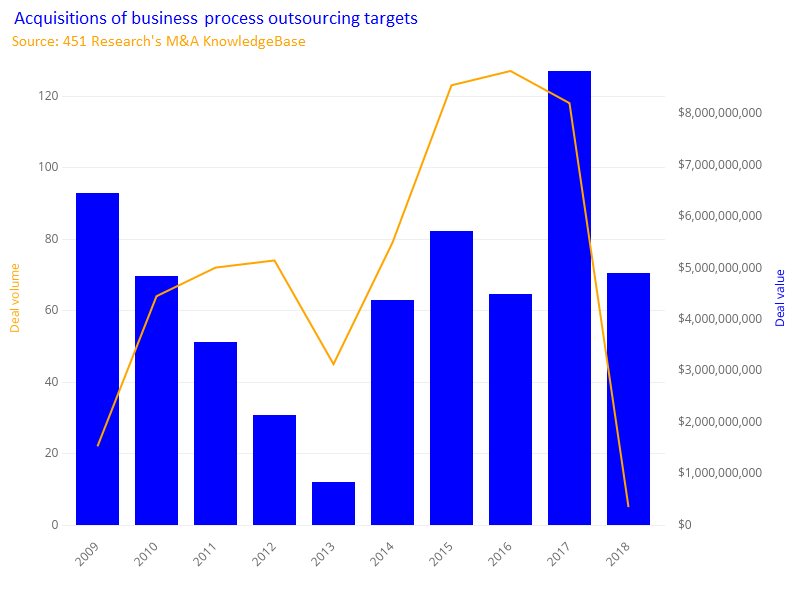

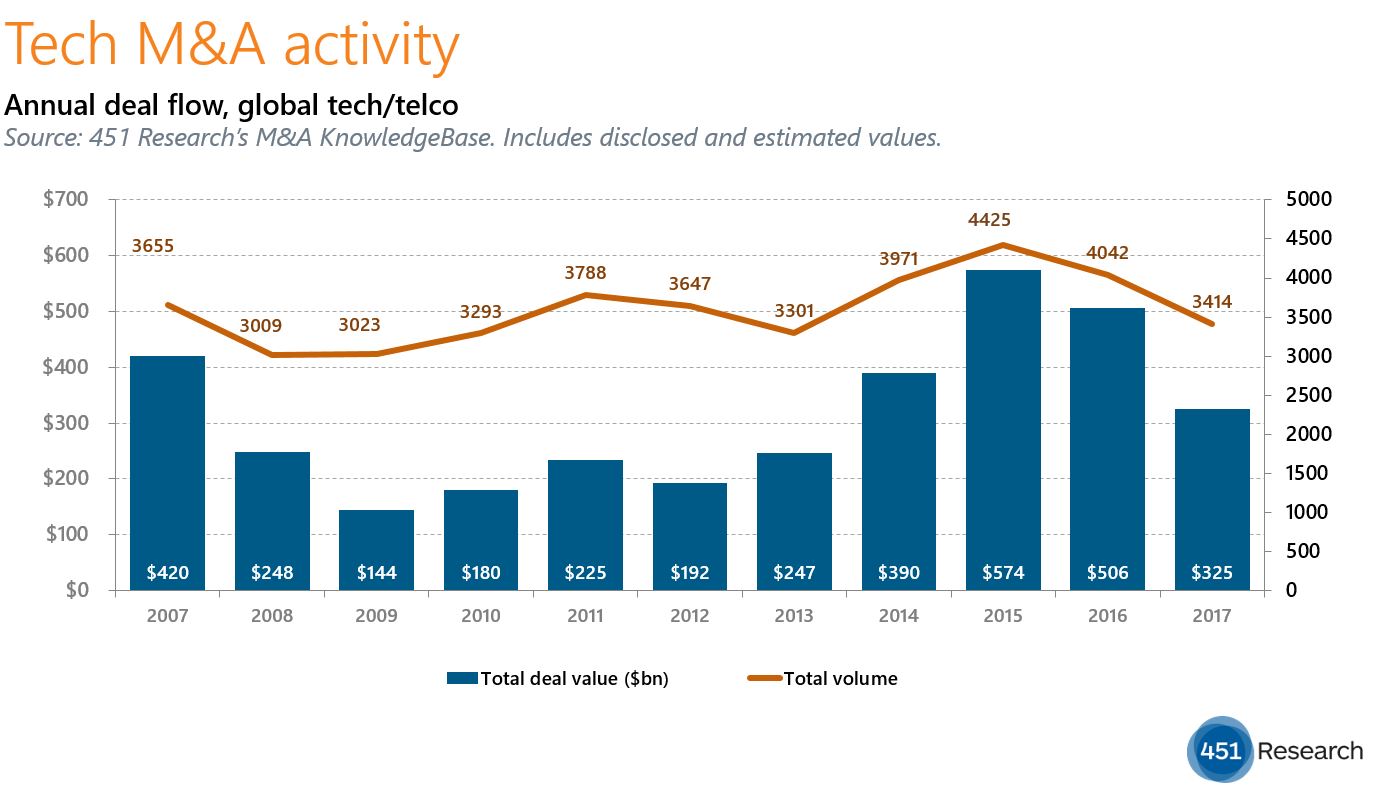

- After tech M&A spending in both 2015 and 2016 topped a half-trillion dollars, what happened that knocked the value of deals in 2017 down to just $325bn?

- Many of the tech industry’s biggest buyers printed only half as many deals as they have in recent years. Is that the new pace of M&A at these serial acquirers, or will they rev up again in 2018?

- The pending tax overhaul will likely add billions of dollars to the treasuries at major tech vendors. Why don’t we think that will necessarily lead to more M&A? If they don’t spend it on deals, what are tech companies going to do with the windfall?

- Which tech markets are expected to see the biggest flow of M&A dollars in the coming year? Enterprise security tops the forecast once again, but what about emerging cross-sector themes such as machine learning and the Internet of Things?

- How did private equity (PE) move from operating on the fringes of the tech industry to become the buyer of record? PE firms accounted for an unprecedented one out of every four tech transactions last year. Why do we think their share of the market will only increase?

- VC portfolios are stuffed, as the number of exits in 2017 slumped to its lowest level since the recession. What challenges loom for startups and the broader entrepreneurial community without the return of billions of dollars from those investments?

- For startups, will venture capital be flowing freely in 2018? Or will the polarized VC market (fewer rounds, but bigger rounds) continue this year?

- Despite nearly ideal stock market conditions, why don’t we expect much acceleration in the tech IPO market in 2018? What needs to happen – to both supply and demand – for the number of new offerings to take off?

For answers to these questions – as well as other factors that will influence dealmaking in 2018 – see our just-published 2018 Tech M&A Outlook – Introduction.