by Brenon Daly

When investors flipped their calendars from October to November, they were also hoping to turn the page on the worries that knocked US stocks last month to their worst monthly performance in six years. They looked through last week’s political instability – the divisive midterm elections in the US, which, appropriately enough, produced a divided Congress – in favor of market stability. Calm had descended on Wall Street once again.

And then came this week. Stability eroded and confidence evaporated, prompting investors to dump stocks in early-afternoon trading today and, even more so, on Monday. Stock market indexes that had hung close to the level where they opened the month in the first week of November suddenly plummeted into the red. Instead of a rebound from October, trading in November has turned into more of the same from last month.

Most market participants track uncertainty through the CBOE’s Volatility Index, which is known as the VIX. (Fast-talking traders shorthand everything.) Without going too deeply into the makeup and implications of the VIX, the index measures investors’ expectations about the direction of stocks. The index tends to move higher when stocks move lower.

We certainly saw that in last month’s bear market, when the VIX surged to roughly twice the level it held in the summer months. And while the so-called ‘fear gauge’ did ease significantly in early November as US equity markets recovered, this week’s rout has spurred it higher. The VIX is one-third higher now than it was last week, and is approaching last month’s levels.

As a mechanical measure of human emotion, however, the VIX has its shortcomings. Its utility is also limited because it is, necessarily, tied to every single tick of the market. That makes it difficult to base long-term strategy – whether a significant investment or a meaningful acquisition – on an index that fluctuates every second.

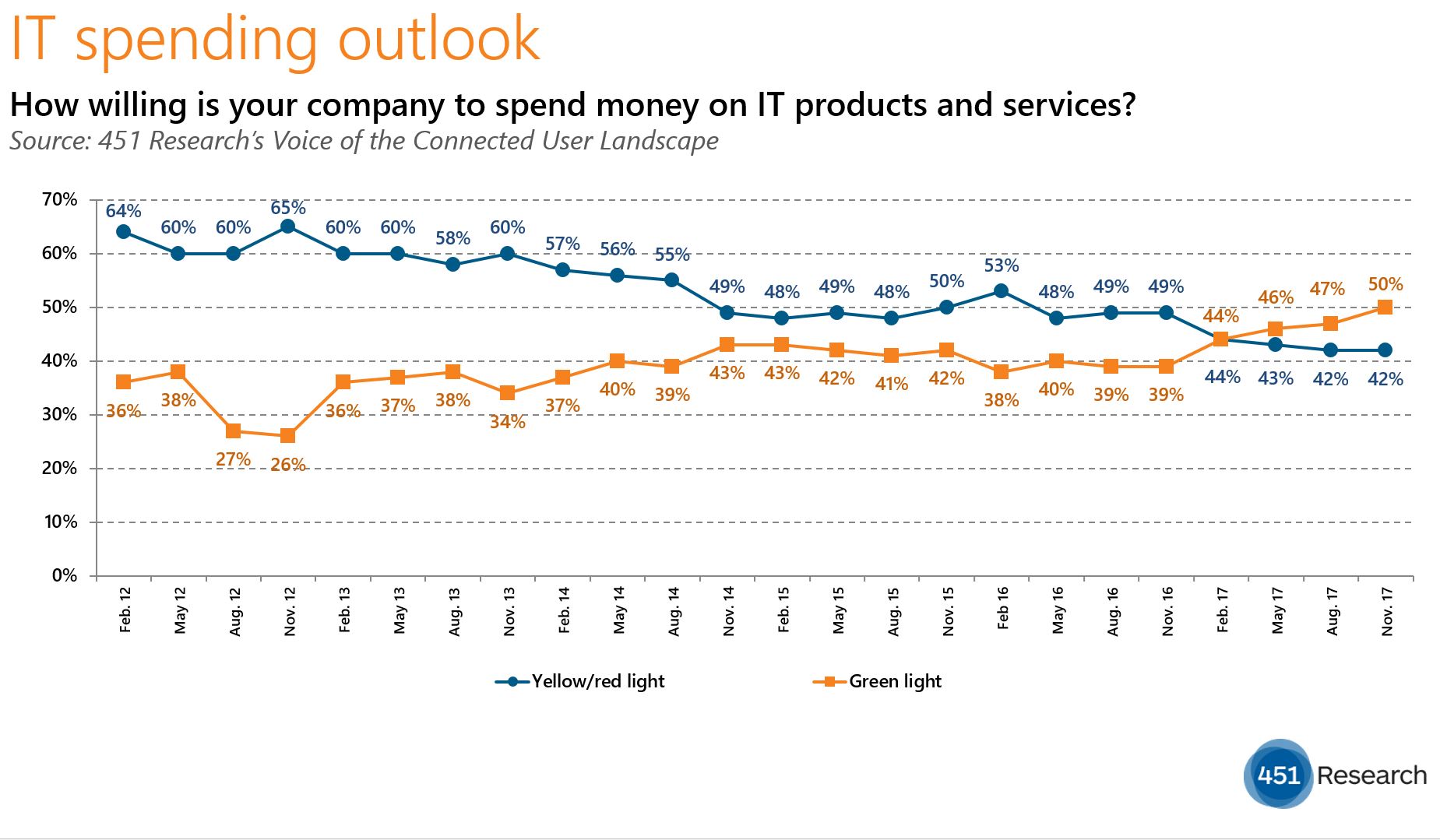

At 451 Research, we have our own version of the VIX. As part of a monthly survey, our Voice of the Connected User Landscape (VoCUL) asks over 1,400 respondents how they feel about the stock market. Specifically, we ask about the all-important sentiment of confidence in the market right now compared with three months earlier. Both the timing and the structure of our question is designed to draw out a more durable forecast than the more-reactive VIX.

So what does our survey say? Given the uncertainty that ripped through Wall Street in October, it’s probably no surprise that investor sentiment deteriorated notably in the latest VoCUL survey. Just one in eight respondents indicated that they had more confidence in Wall Street now than in August, when the stock market was roughly 10% higher. The most recent outlook – with the bearish views outnumbering the bulls almost three to one – is among the dourest outlooks of the past three years.