by Brenon Daly

Dynatrace’s IPO represents the third major transition in recent years for the application performance management (APM) company. Like the other two, today’s shift has proved wildly lucrative. Dynatrace created more than $7bn in market value as it moved from private equity to public trading.

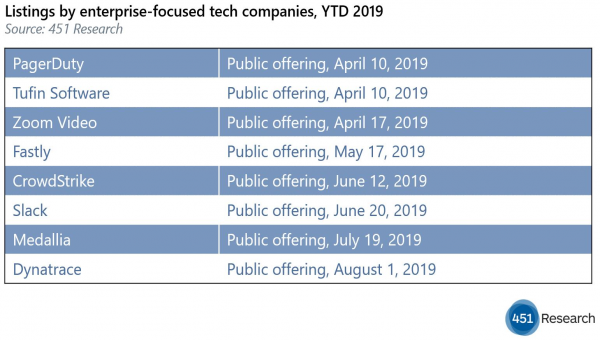

Although not unprecedented, Dynatrace’s partial swapping out of financial sponsor Thoma Bravo for Wall Street investors is still somewhat unusual. (Post-offering, the PE firm still owns about 70% of Dynatrace.) By our count, just three of the two dozen enterprise-focused technology vendors, including Dynatrace, that have gone public in the US since the start of 2018 have come from PE portfolios. Dynatrace raised roughly $570m in its offering, some of which will go toward paying down its nearly $1bn in debt, which, again, stands in contrast to the typical VC-fueled growth for most tech IPO candidates.

In many ways, the partial change in ownership for 14-year-old Dynatrace is the culmination of the other two changes, the first being a technology overhaul followed by a shift in business model. As we noted in our full report on the IPO, Dynatrace revamped its product a half-decade ago, integrating all of its monitoring into a single platform. (It no longer sells its legacy product, which it refers to as ‘classic,’ except to existing customers.)

As part of the transition to a platform, Dynatrace also changed how it sold its product, as well as how it accounted for those sales. Gone were licenses, in favor of subscriptions. And while the company has undeniably made progress in its transition to a new, more valuable business model, it has also been undeniably aided in its efforts by a rather expansive definition of ‘subscription’ revenue.

Accounting purists might have a hard time signing off on Dynatrace’s practice of including term and perpetual licenses, as well as maintenance and support revenue, all as subscription revenue. Basically, the company lumps all sales of its non-classic product – regardless of whether it is true SaaS or license-based – into the subscription line on its income statement.

Our quibbles about accounting are rather minor, and certainly didn’t stand in the way of professional investors, who have long since given up on GAAP, from rushing to buy newly issued shares of Dynatrace. The stock surged 60% shortly after its debut on the NYSE. With roughly 286 million (undiluted) shares outstanding, Dynatrace began life as a public company with a value of $7.4bn. That’s one-third more than the current value of APM rival New Relic, which has been public since Dynatrace first started its product transition some five years ago.