by Brenon Daly

At its most basic, an acquisition is just the end result of strategy and structure. The first part of the equation (strategy) tends to command most of the attention, while the structure of a transaction often gets dismissed as mere ‘paperwork.’ It’s a bit like a wedding. Most of us don’t celebrate the signing of a marriage certificate – a document that, like an acquisition agreement, is legally binding. No, the reason we get together to sappily toast the couple and awkwardly dance to ‘Brick House’ is to celebrate the idea of two people joyfully spending their lives together. In both marriage and M&A, the grand vision for the union is more emotionally satisfying than the nuts and bolts of the agreement.

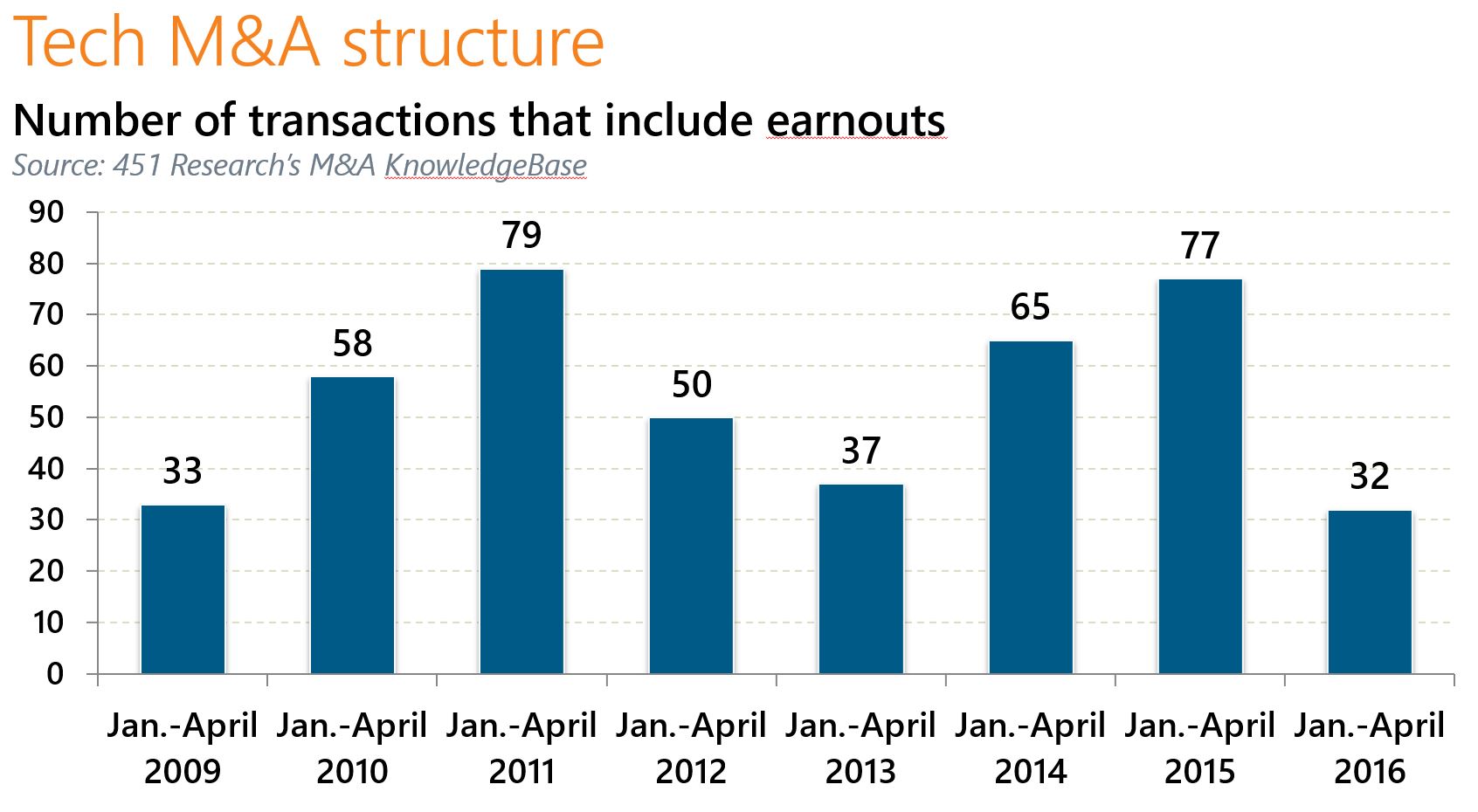

Yet, terms matter. They not only shape specific deals and the ultimate return on those transactions, but also provide useful indicators about the broader market. Consider the case of earnouts, which are additional payments an acquirer makes if a target company hits certain milestones. Typically, as any dealmaker can tell you, earnouts are used to bridge valuation differences.

So, what to make of the fact that earnouts have fallen dramatically out of favor? According to 451 Research’s M&A KnowledgeBase, so far this year dealmakers have included the provision just half as often as the same period in each of the two previous years. Earnouts haven’t been used this sparingly since the recession year of 2009.

One possible reason for the sharp decline is that buyers no longer feel the need to stretch on valuation. That certainly came through in the M&A Leaders’ Survey from 451 Research and Morrison & Foerster, where a record two-thirds of acquirers and their advisers predicted that private company acquisition valuations would be coming down for the remainder of 2016. And the fact that buyers no longer feel they need to include as many financial kickers as they once did to purchase the companies they want suggests that they have the upper hand in negotiations right now.