by Scott Denne

The rising tide of 2018’s record software M&A market gave way to a top-heavy 2019 as fewer business application vendors fetched a 10-figure price but a record number nabbed 11 figures. And while the size of the market shrank a bit from last year’s high as both strategics and sponsors slowed their spending, the total stands well above the deal value and volume seen in a typical year. Despite the decrease in overall deal value, acquirers continued to pay premium multiples for those assets they did purchase, something they’re less likely to do in the new year.

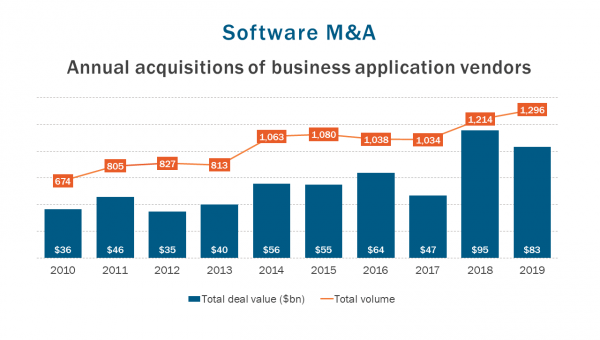

According to 451 Research’s M&A KnowledgeBase, acquirers in 2019 bought a record 1,296 application software companies worth $83.2bn, about $12bn less than the previous year. A dramatic drop in transactions valued north of $1bn led the decline in spending. Yet the biggest software deals got bigger. Two acquisitions – Salesforce’s $15.5bn reach for Tableau and Hellman & Friedman’s $11bn Ultimate Software take-private – passed the 11-figure mark in 2019, something that only one other application vendor (Autonomy) had done since the start of the decade.

While only half as many application providers sold for $1bn or more in 2019 as did a year earlier, the 15 transactions that went off in 2019 stand as the second-highest total, according to the M&A KnowledgeBase. In other words, it may be more accurate to view 2019 as an inevitable decline that followed a sudden surge in 2018. In each year since 2010, we’ve consistently recorded about 12 application software deals valued at or above $1bn, meaning that 2019 was notably high, yet well below the 30 we saw in 2018.

And while the number of $1bn software transactions shrank, prices didn’t. The annual median for such deals finished a hair above 7x trailing revenue, the same level as the previous year, our data shows. Who was willing to pay those prices shifted in 2019, however. While private equity firms paid that same multiple in 2018, the median price paid by sponsors to acquire software companies for 10 figures declined a full turn last year. Strategic buyers moved in the other direction, paying a 9.3x median as they continued to pay higher prices in each of the past few years.

Although valuations for application software vendors held up amid a decline in overall spending last year, prices could well begin to fall in 2020. That’s the outlook of respondents to our M&A Leaders survey in October, where they projected a drop in private company valuations at a rate of five to one. Moreover, 2020 starts off with a tougher macro environment than its predecessor. In that same survey, nearly two-thirds of respondents (61%) said that ‘fear of a recession’ could weigh on deal flow in the coming 12 months.

Figure 1: