by Brenon Daly

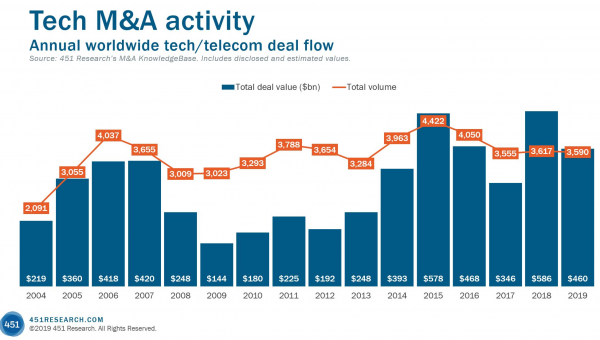

Tech M&A spending in 2019 dropped nearly 20% from the previous year’s record level, as mainstay acquirers stayed away, and an up-and-comer came up short. The combination of the tech industry’s bellwethers not buying and buyout shops slowing their record roll sank the value of tech and telecom acquisitions announced around the world last year to $460bn, according to 451 Research’s M&A KnowledgeBase.

Still, 2019 stands as the fourth-highest annual total since the internet bubble collapsed. The fact that last year hit such heights is rather remarkable, given that it was missing the main engine that has powered tech M&A over the past decades: big-cap acquirers.

As an indication of that, consider that our M&A KnowledgeBase shows that Oracle, Microsoft, IBM and SAP, collectively, did not put up a single billion-dollar print in 2019. It was the first time since 2003 the always-hungry quartet haven’t been in the ‘three comma club.’ Up until last year’s notable absence, the big buyers had been averaging three or four acquisitions between them valued at more than $1bn each year.

Further, our data indicates the ‘first gen’ quartet put up just half the number of overall deals in 2019 that they had been averaging over the past 15 years. It was as if the old guard, having shaped and driven the broader tech M&A market in the 2010s, stepped aside as the curtain came down on the decade. Last year marked the end of an era.

As that transition was playing out in the ranks of the strategic acquirers, the other main buying group was also facing changes of their own. Private equity (PE) firms announced fewer tech transactions in 2019 than they did in 2018, according to our M&A KnowledgeBase. That marked the first decline in deal volume in six years for deep-pocketed financial buyers, which had been the only ‘growth sector’ in the overall tech M&A market for the past few years.