by Michael Hill

A years-long increase in SaaS acquisitions by private equity (PE) firms is flattening out. Yet sponsors are spending far more than in the past for those targets – typically paying more for SaaS vendors than strategic acquirers do – as businesses shift more of their budgets toward hosted software offerings.

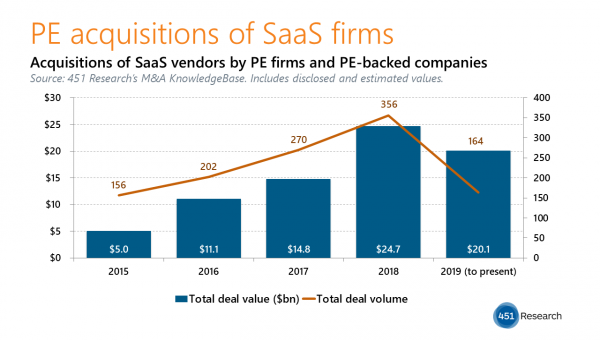

According to 451 Research’s M&A KnowledgeBase, PE shops have bought roughly the same number of SaaS targets as this time last year, following several years of increasing the volume of those deals 25% or more each year. Despite that, sponsors have spent more than $20bn on SaaS acquisitions so far in 2019, compared with $24.7bn for the entirety of 2018. Much of the jump stems from Hellman & Friedman’s $11bn take-private of Ultimate Software. Still, even without that transaction, PE firms have spent nearly three times as much on SaaS purchases this year as they did during the same period last year.

And 2019’s larger deals are coming at a premium. So far, the median trailing revenue multiple for a SaaS target in a sale to a buyout shop or PE portfolio company stands at 4.9x, a turn higher than any full year this decade. Our data also shows that 2019 marks the first year that PE firms have paid higher multiples than strategic buyers, whose acquisitions of SaaS vendors carry a 4.5x median multiple this year.

The increase in valuations comes as businesses are pushing more of their IT budgets into SaaS. According to our most recent Voice of the Enterprise: Cloud, Hosting and Managed Services, Budgets & Outlook – Quarterly Advisory Report, 67% of respondents expect to increase their spending on SaaS this year. What’s more, 38% expect SaaS to be their largest area of spending growth among cloud and hosted services.