by Scott Denne

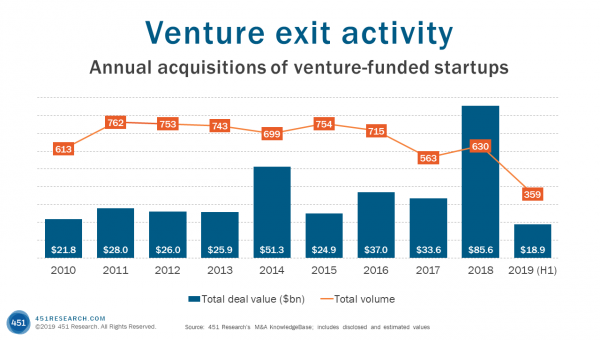

Although unlikely to match last year’s record haul in dollar terms, the liquidity in this year’s VC exit market is more evenly distributed. Through the first half of 2019, more venture-backed companies are on pace to exit than in any year since 2016, shaking off a years-long decline in exit volume. At the same time, blockbuster deals are trending down as many of the venture community’s most reliable buyers have stayed out of the market and some of the most promising vendors opt for public listings.

According to 451 Research’s M&A KnowledgeBase, 359 venture-funded companies were acquired through the first half of 2019, a pace that’s up 15% from last year, which was the lightest year for venture exits, by volume, since 2010. So far, sales of VC-backed tech vendors fetched just $18.9bn, compared with $85.6bn in all of 2019. Although exits are set to pull in less than last year, sales of companies from venture portfolios, if the current pace holds, would generate more than all but two years in the current decade.

Even as more deals print, the typical value of those transactions holds steady from last year’s level. The median deal value of a 2019 venture exit (via M&A) stands at $100m through the first half of the year, slightly down from where it finished last year, and far higher than all other years this decade. It’s a decline in big-ticket acquisitions that’s weighing on this year’s total deal value. So far, only two venture-backed vendors have sold for more than $1bn, compared with 13 in all of last year. Put another way, if past is precedent and 2019 ends with a total of four $1bn VC company sales, there will have been as many $1bn-plus exits in 2019 as there were $5bn-plus exits a year earlier.

Still, it’s not likely that acquirers have lost interest in inking substantial purchases of VC-backed targets. After all, the rise in the stock market through this year has bolstered valuations of many would-be buyers and should make them more willing to do big prints. Instead, venture-backed startups have more exit options and are getting more expensive. The multiple Google paid in its $2.6bn pickup of Looker speaks to that (subscribers of the M&A KnowledgeBase can see that multiple here). Instead of selling, many of the most attractive targets are eyeing the public markets, where, as we discussed in a recent report, many new issuers are fetching multiples north of 40x trailing revenue.